Hey readers, do you have extra money and not sure what you should do with it? Well today let’s discuss what you could do with that extra money.

If you have an extra RM1,000 every month, you may start thinking about how to make better use of it. Instead of letting the money sit in your bank account, you can put it to work through saving or investing.

Before investing, however, you should first build an emergency fund.

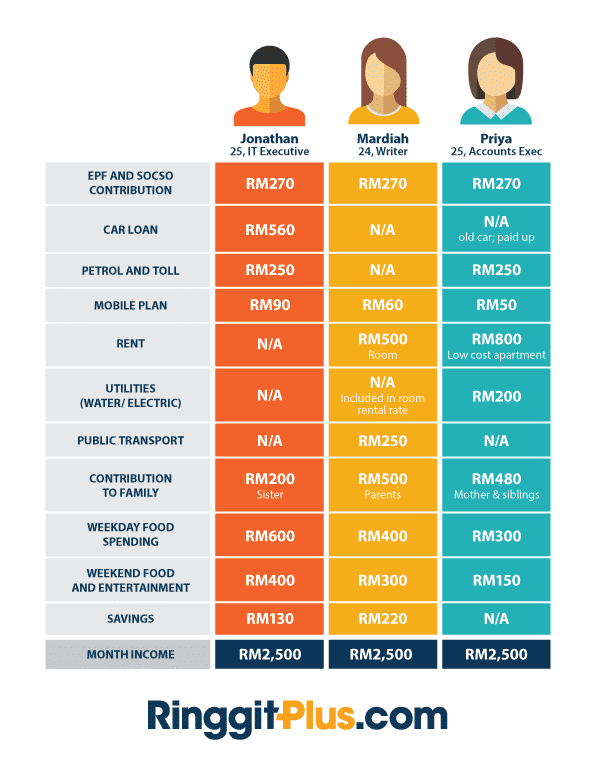

An emergency fund should cover about three months of your basic expenses. For example, if you spend around RM2,500 per month on rent, food, transportation, and daily costs, you should aim to save about RM7,500.

This money should stay in a safe and liquid place, such as a savings account or cash management fund. The goal is simple: if something unexpected happens — like a medical emergency or job loss — you will still have money to cover your expenses.

Once your emergency fund is ready, you can start thinking about how to invest your extra RM1,000 each month.

Here are some of the best way to invest on Extra RM1000

Employees Provident Fund (EPF)

The Employees Provident Fund (EPF) was introduced in 1951. It is a retirement savings system for private-sector employees in Malaysia.

Recently, EPF announced a 6.15% dividend for both the conventional and Syariah accounts. Over the past 10 years, the conventional account has delivered an average return of 5.88% per year. This is higher than Malaysia’s average inflation rate of about 2%.

Malaysians can also make voluntary contributions to EPF. The minimum amount is RM10, and the maximum is RM100,000 per year.

However, EPF is mainly meant for retirement savings. Most of the money in Account 1 cannot be withdrawn until age 55. Account 2 allows some withdrawals, but only for specific purposes such as housing or education.

Because of this structure, EPF is best for people who want stable long-term savings, even though it offers less liquidity compared to other investments.

| Pros | • Historical great dividend returns of at least 5-6% • Low Risk |

| Cons | • Locked-in period at least until 55 years old for Retirement Fund • Limited Growth |

| Average ROI | 5.88% return on 10 years average |

Unit Trust Fund

Unit Trust Fund works as having pool money from multiple investors and investing it into a diversified portfolio managed by professional fund managers. The key difference between each fund lies in its investment objective, risk level, and asset allocation strategy.

Some of the well-known unit trust options in Malaysia included :

- ASM (Amanah Saham Malaysia) – open to all Malaysians

- ASB (Amanah Saham Bumiputera) – for Bumiputera investors

- Touch ‘n Go+ investment funds

| Pros | • Low Volatility • Managed by professional fund managers. |

| Cons | • Certain funds (e.g., ASM), unit availability may be limited due to quota restrictions. •Returns are generally moderate and may not significantly outperform inflation over the long term |

| Average ROI | Amanah Saham Malaysia generate around 4.45% for the past 5 years |

| Place to Invest (Recommended) | • Amanah Saham (ASNB) • TouchnGO+ |

ROBO Advisor

ROBO Advisor act as digital investment platform that is built on a system of algorithms and data to invest on behalf of customers.

For example, platforms like StashAway allow you to start investing in just a few steps. First, create an account and complete a short risk assessment. This helps the platform understand your investment profile. Then, deposit your RM1,000 through an online transfer

| Pros | • Globally diversified portfolio • Automatically rebalanced |

| Cons | • Portfolio value may fluctuate significantly during downturns depending on preferences |

| Average ROI | Depends on the investment portfolio selected and risk level. |

| Place to Invest (Recommended) | • StashAway • Versa |

Gold

Gold has long been considered a safe-haven asset. Investors often turn to gold during periods of economic uncertainty or political instability.

Over the past 10 years, gold has delivered an estimated 13.6% CAGR as of 2025. During certain periods, this performance even exceeded the returns of the S&P 500.

Recently, geopolitical tensions, wars, inflation concerns, and central bank policies have increased demand for gold.

However, gold has an important limitation. Unlike stocks or bonds, it does not generate income or dividends. Returns depend entirely on price increases, which can be volatile in the short term.

| Pros | • Safe-haven asset during geopolitical uncertainty • |

| Cons | • Does not generate dividends or cash flow •Price can be volatile in short-term movements |

| Average ROI | •Approximately 10–14% CAGR globally for the past 10 years |

| Place to Invest (Recommended) | • Bursa Malaysia Gold ETF • Maybank Gold |

Stock market

With technology growing, it is getting easier for us to access both Malaysia and Global Stock Market investment from our own smartphone.

Today, technology makes it easy to invest in both Malaysian and global stock markets using a smartphone.

Investors can buy stocks listed on Bursa Malaysia as well as major global markets like the S&P 500, Nasdaq, and Hang Seng Index.

Besides buying individual stocks, investors can also invest in Exchange Traded Funds (ETFs). ETFs allow you to invest in a basket of companies within one fund. Because of this, ETFs offer diversification and lower investment costs.

| Pros | • Easy access to local and global markets via online brokers • Dividend income for generating more cash flow (Dividend-paying companies) •Potential for higher long-term returns |

| Cons | • Market volatility (prices can drop sharply during recessions or crises) •Requires research and monitoring if investing in individual stocks |

| Average ROI | •S&P500 Index 11% CAGR Return for the past 10 years |

| Place to Invest (Recommended) | • MooMoo Malaysia • Webull Malaysia |

I will explain a covered blog about investing and how to invest in stock market for both different market perspectives.

Cryptocurrencies

The cryptocurrency market has changed significantly over the years.

At first, many people believed crypto was only a short-term trend. However, adoption has grown rapidly. Today, many institutions and governments are paying closer attention to digital assets.

In my own portfolio, I only hold the two largest cryptocurrencies: Bitcoin and Ethereum.

Bitcoin is often called “digital gold” because it is mainly used as a store of value. Ethereum, on the other hand, supports smart contracts and decentralized applications.

Both cryptocurrencies have survived multiple market cycles and crashes. That is why I continue to hold them.

| Pros | • High growth potential • Increasing global adoption and institutional interest •Can act as a diversification asset in a portfolio |

| Cons | • High volatility (prices can swing 10–20% in days) •Requires strong emotional discipline during market crashes |

| Average ROI | • CAGR of 19.3% for the past 5 years |

| Place to Invest (Recommended) | • Hata • LUNO Malaysia |

My POV

Every investment vehicle exists to serve a different type of investor.

There is no single “best investment.” The right choice depends on your financial situation, risk tolerance, and life stage.

Risk tolerance also changes over time. It depends on income stability, financial commitments, and personal goals.

As a fresh graduate early in my career, I currently have fewer financial obligations. Because of this, I am more comfortable allocating part of my capital to higher-risk investments, such as stocks and cryptocurrencies.

So here is my suggestion for you on three different examples.

| Example 1 | Example 2 | Example 3 | |

| Someone With | Conservative Allocation | Moderate Allocation | Aggressive Allocation |

| Characteristics | Unstable income Low emergency savings Low risk tolerance | Stable income Basic emergency fund Medium risk tolerance | Early career Growing income High risk capacity |

| RM1000 Investment Options | RM500 → Emergency savings RM300 → ASNB / Cash fund RM200 → ETF | RM700 → Global ETF / Robo RM200 → EPF voluntary RM100 → Crypto | RM700 → Growth ETFs / US stocks RM300 → Crypto |

Remember DYOR (Do your own research) before investing something. Hope this article helps you so you can find the best way to use an Extra RM1,000 in Malaysia.

Kaching$$ !!